A 2020 that no one could have foreseen is drawing to a close with the bulk wine market active but less active than it was in late summer/early fall when smoke exposure concerns joined with heightened off-premise demand to stimulate a buying frenzy. The market picture is now difficult to summarize because it is so granulated: everyone – buyers and sellers alike – are tentatively trying to navigate their own way through a landscape with little forward visibility.

A 2020 that no one could have foreseen is drawing to a close with the bulk wine market active but less active than it was in late summer/early fall when smoke exposure concerns joined with heightened off-premise demand to stimulate a buying frenzy. The market picture is now difficult to summarize because it is so granulated: everyone – buyers and sellers alike – are tentatively trying to navigate their own way through a landscape with little forward visibility.

On the one hand, the commencement of COVID-19 vaccine rollouts in some parts of the world raises the prospect of a more ‘normal’ 2021 – at least by the second half of the year. But on the other hand, the recent reimposition of a strict stay-at-home order across most of California is a reminder that the virus is still very much with us. Once the virus is under better control, if not eliminated, the focus will turn to the economic fallout.

According to Nielsen data, off-premise domestic table/sparkling wine sales in the US have continued strongly, with sales up 17% by value in the four weeks ending October 31 versus the same period of 2019. Consistent statistics such as these have led to a suggestion that total wine sales in the US could be up this year by volume, with the off-premise managing to offset the on-premise’s cratering, but this is based on the assumption that this year’s off-premise OND sales will follow the traditional trend – something that cannot be taken for granted in this, the most untraditional of years. Further data suggests the pandemic has sped-up a pre-existing trend towards online shopping: Up to a quarter of US consumers have now bought wine online, either direct from wineries or from retailers.

We have seen a slight rise in off-premise pricing as on-premise suppliers redirect their wines into grocery stores. There is a big question mark as to how sustainable margins gained from off-premise sales are for many Coastal wineries in the longer term. And redirecting the wine into the off-premise, often with a much-reduced price tag on the shelf, can run the risk of brand devaluation in the longer term.

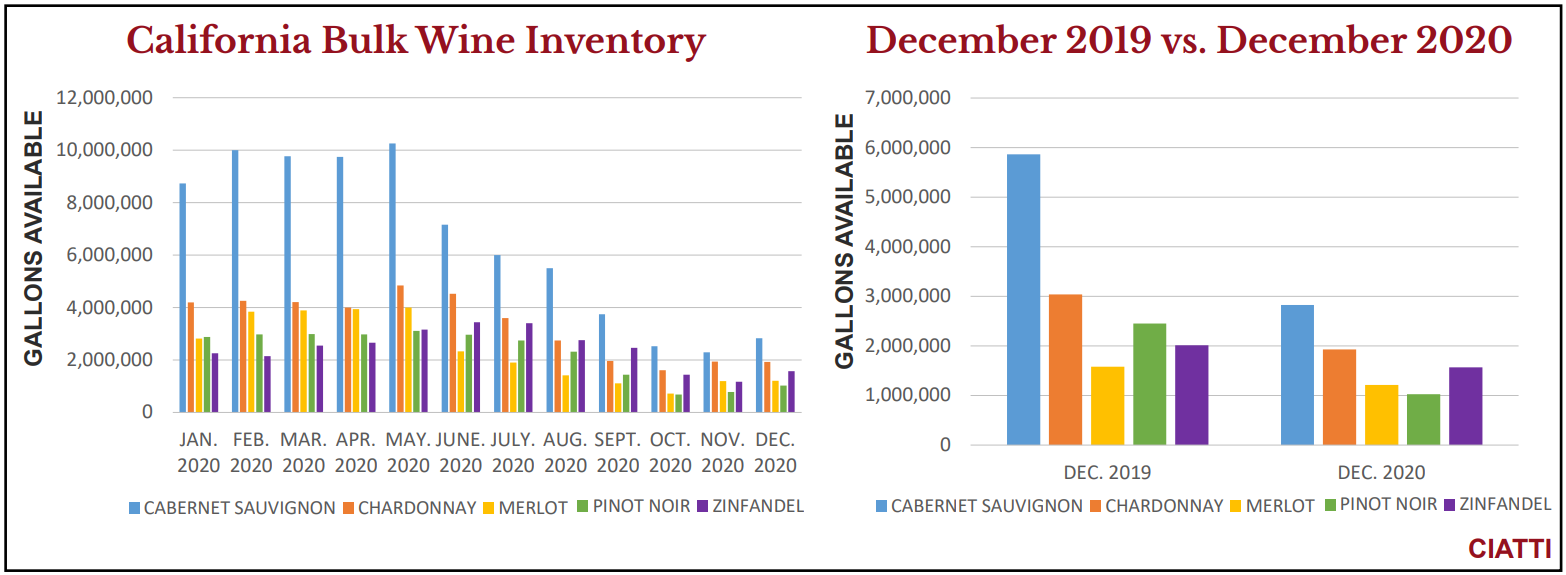

This year has shown how quickly things can change: As the inventory barometer in this month’s report illustrates, we estimate current Cabernet inventory is now approximately half what it was in December 2019, while the respective inventories of Chardonnay, Merlot, Pinot Noir and Zinfandel are also significantly less than they were to varying extents. Supply of the 2019 vintage is now very limited – and often high in price – and there is little clarity on 2020 vintage availability levels due to the lighter than average crop and any potential smoke impact. Together with this supply instability, the difficulty in making confident sales projections due to COVID-19 means there is demand instability as well. Read on for the latest on California’s bulk wine and grape markets.

As the market currently stands, then, it pays even more to be in dialogue with your broker as we continue to do our best to help you navigate the market. Do reach out to us with your bulk wine samples and the grapes you will have for sale in 2021. Likewise, let us know what bulk wine or grape needs you have. In the meantime, everyone at Ciatti wishes you and yours a very Happy Holidays and a prosperous – and healthy – New Year.