Filter Post Type

NewsVideoProductEventLink

Sort:

Relevance

1–10 of 57

by Steve Chapman, World Cooperage Account Manager China is a land of contrasts, especially when it comes to the different vineyard regions spread across this vast country. From the wet and humid east coast, to the temperate central regions, and the arid and cold northwest, there is an incredible spectrum of growing conditions. Harvest Time In Xinjiang Provence This variation in growing conditions presents a multitude of challenges to both viticulturalists and winemakers. As coopers, we also have to ensure we are supplying the correct barrel type suitable for the different regions and wine styles. Luckily, we have built great relationships with our customers over the years. Assisted by our long time friend and Agent, Michael Zhang, we have seen some stunning results. In fact, one of our customers, Canaan (north of Beijing), has produced some outstanding Cabernet Sauvignon and Chardonnay by adopting modern vineyard practices and incorporating appropriate barrel choices in t

00

October 21, 2025

Natural cork stoppers are often viewed as a pricier alternative to other closures - such as aluminum or plastic stoppers - and even other cork closures, like microagglomerate and colmated cork stoppers. However, the fact that it represents a bigger investment doesn’t mean choosing natural cork stoppers doesn’t pay off. There are plenty of reasons to pick natural cork stoppers in detriment to synthetic alternatives. Let’s look at some of them. Natural cork is associated with high-quality wine A study conducted in Italy confirmed that wine drinkers experience a higher cognitive and emotional response to smelling, tasting, and even listening to a wine sealed with a cork stopper than they do with a wine sealed with a screw cap. In fact, on a global level, cork is associated with high-quality wine, which makes it the preferred sealant for many consumers all around the world. This becomes especially interesting when you consider that consumers in high-income countr

00

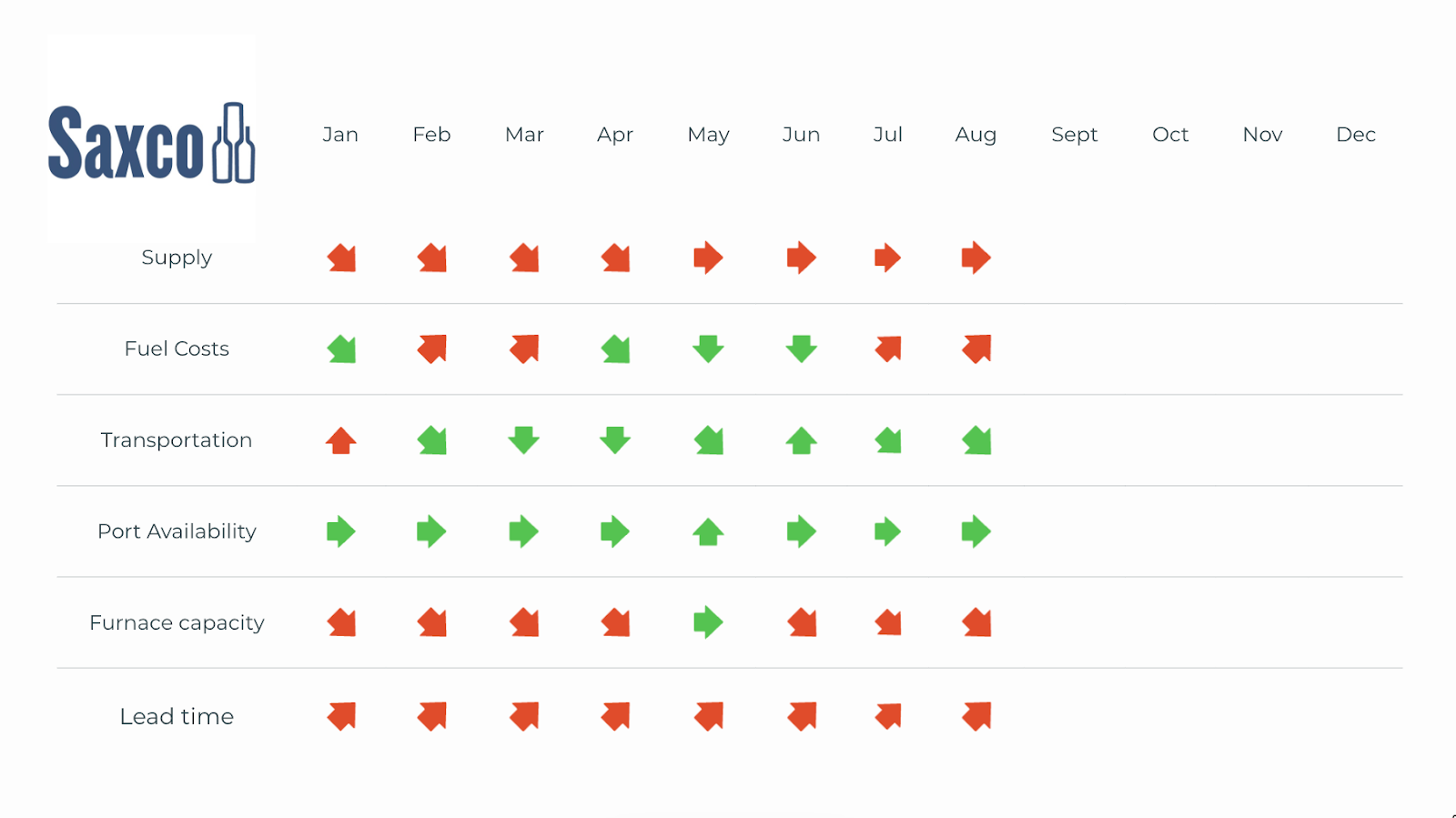

July's supply chain landscape feels deceptively calm, but the undercurrents are shifting. Fuel costs ticked upward again – $3.599 to $3.779 per gallon – putting quiet pressure on logistics, even as transportation costs eased with the surprising disappearance of peak season surcharges. That dip is a welcome but likely temporary reprieve. On the production side, capacity continues to tighten: OI’s Portland plant has officially closed, and two additional furnaces are scheduled to go offline, which continues to raise concerns about domestic supply heading into the back half of the year. Lead times have not budged from June’s elevated levels, but with fewer furnaces online, we are likely to see that stress compound by fall. Ports remain neutral, and overall supply feels steady – but for now, it is a still surface over increasingly strained infrastructure. Tariff watch: The rules are changing The new US tariff rates announced on July 31 mark a signifi

00

July 17, 2025

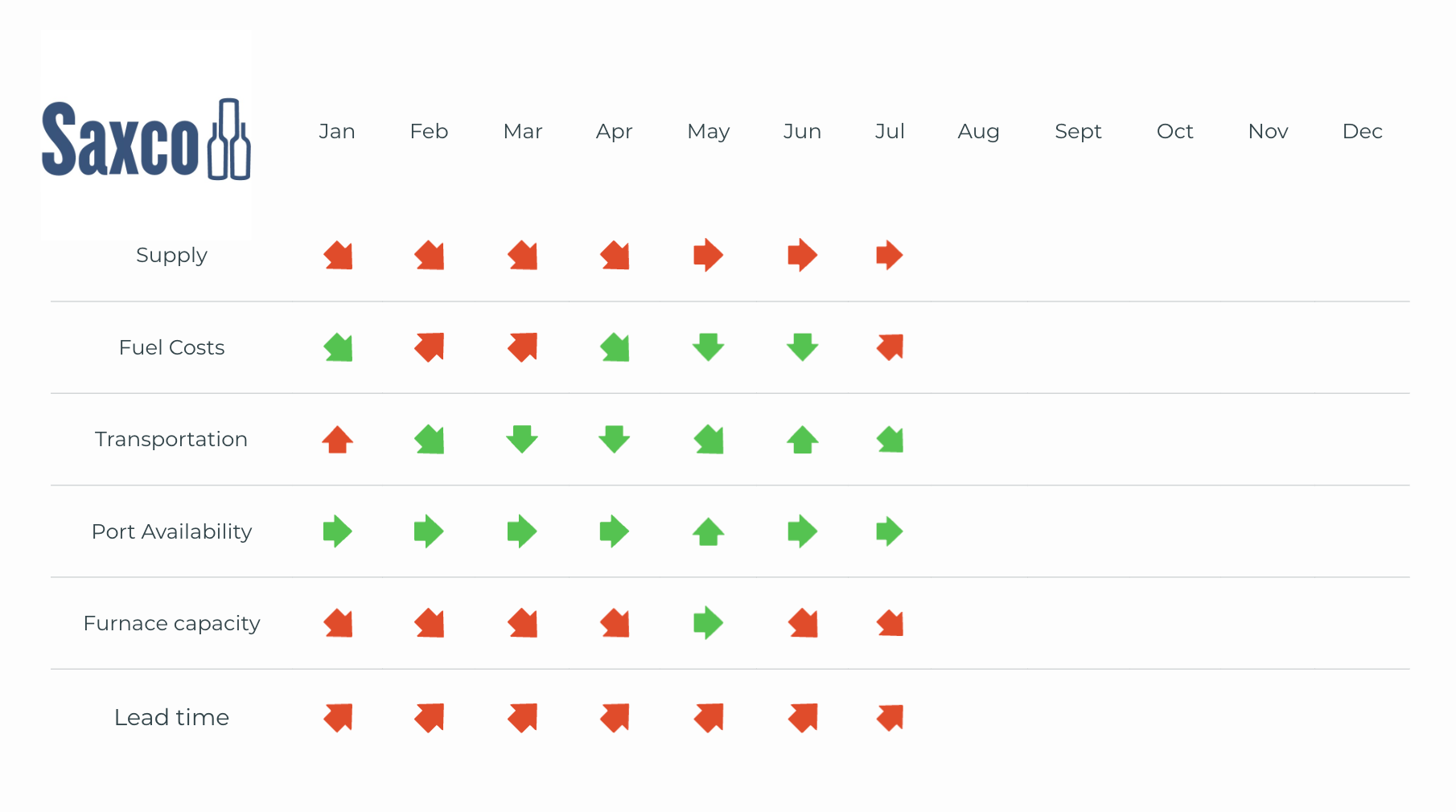

Packaging supply stable, but uneasy While June ushered in a more stable rhythm after May’s tariff-driven frenzy, underlying uncertainty continues to shape planning, procurement, and pricing across the packaging and logistics landscape. Supply remains steady across most categories, but stability doesn’t mean simplicity. US glass manufacturers, in particular, are contending with a mismatch between output and demand. Inventories have piled up amid sluggish ordering, especially from wine producers still reeling from compressed consumer spending and slowing DTC velocity. With tanks and warehouses more full than empty, some domestic furnaces are now eyeing Q3/Q4 production pauses as a measure to rebalance. After a brief reprieve in May, diesel prices rose again in June, increasing from $3.499 to $3.599 per gallon, a continued reflection of the volatile energy market. According to the latest Deloitte economic outlook, while core inflation is showing signs of moderation, ener

00

May 22, 2025

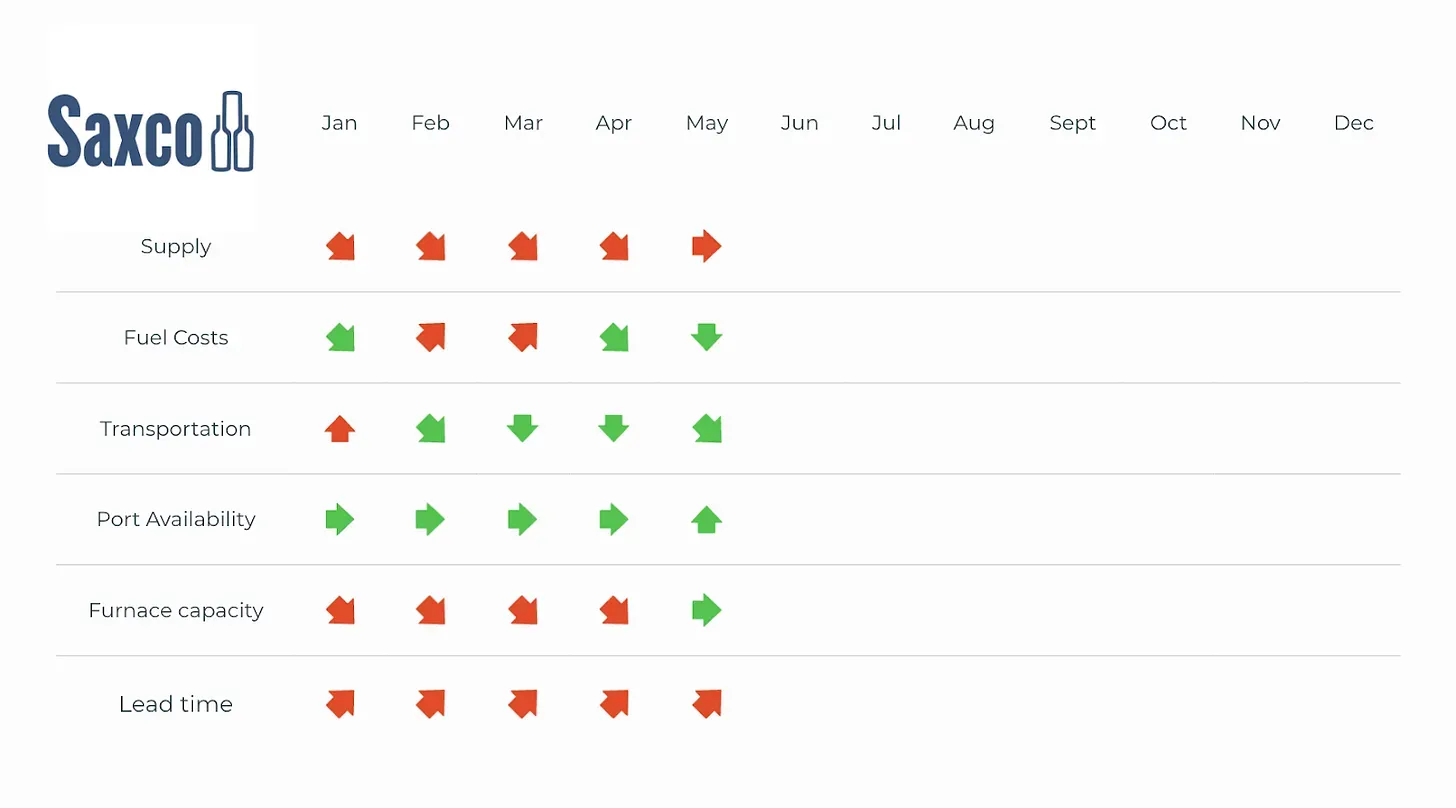

In recent years, US trade policy developments – including broad tariffs and anti-dumping/countervailing duties – have disrupted global supply chains and increased costs across multiple industries. The wine and spirits sector, in particular, continues to experience the ripple effects of trade tensions involving key packaging sources such as China, Mexico, and Canada, along with ongoing tariffs on aluminum and steel. On April 2, 2025, President Trump invoked emergency trade powers under the International Emergency Economic Powers Act (IEEPA), imposing a 10% “baseline” IEEPA tariff on most imported products from most countries, effective April 5. Higher tariff rates on imports from 57 countries were temporarily suspended for all but China, providing a 90-day reprieve. Meanwhile, China was subjected to 125% IEEPA reciprocal tariffs plus 20% IEEPA “fentanyl” tariffs, as well as any other applicable tariffs, such as the 25% China Section 301 tariffs initia

00

Global wine consumption in 2024 is estimated by the Organisation of Vine & Wine (OIV) to have reached 214.2 million hectolitres, down 3.3% versus 2023 and the lowest level since 1961. In its recently-published 2024 industry report, the OIV attributed the decline in consumption – which has “followed a relatively steady trajectory since 2018” – to significantly reduced Chinese demand and the post-pandemic inflation surge which, although having cooled since 2023, still restricts consumer purchasing power to this day. Elevated input costs have made it harder for wine to compete against alternative beverages able to charge a lower price per unit of alcohol. The OIV estimated global production in 2024 at 225.8 million hectolitres, 4.8% down versus 2023 and, again, the lowest level since 1961. This is attributable to climactic conditions but also market adjustments, as vineyards get mothballed or pulled out altogether in response to low winegrape demand. Glo

00

The Northern Hemisphere harvests are in their closing stages and all have experienced shortfalls to varying extents. France is the headline-maker, suffering a shortfall large enough to hand over its rank as the world’s secondlargest wine producer to Spain. The assumption is that the crop in southern France was down 40% versus the average and as much as 50-70% down on the white varietals. The shortfalls elsewhere are not so stark: Italy expects a 9% drop from its 2020 figure, with some September rains helping late maturation in Veneto, Puglia and other regions; Sicily’s crop was in fact up versus the prior year. The La Mancha region of Spain, meanwhile, could see a drop from the multi–year average of approximately 20%. Bulk prices have risen significantly in France, enabling Spanish pricing to move up behind. Spain’s aggressive 2020 vintage pricing is now especially unsustainable for suppliers given recent big increases in dry-good prices and energy bills.&

10

April 15, 2021

Two major milestones mark the beginning of 2021 in the Chinese market: the transformation of its sales office into a distribution subsidiary, and the launch of a new brand in China. April 15th, 2021 – Viña Concha y Toro took another step in its roadmap with the launch of two key initiatives for its commercial […] The post Viña Concha y Toro Presents Flagship Projects to Consolidate Its Commercial Strategy and Strengthen Its Positioning in China appeared first on Wine Industry Advisor. Url:https://wineindustryadvisor.com/2021/04/15/vina-concha-y-toro-presents-flagship-projects?utm_source=rss&utm_medium=rss&utm_campaign=vina-concha-y-toro-presents-flagship-projects Published Date:Thu, 15 Apr 2021 20:27:36 +0000

10

An unseasonably damp summer in many growing areas of Chile (a rainy January followed by nearly three weeks of mist/fog in February) and Argentina (10 weeks or so of lingering rainfall) has raised concern about their respective 2021 vintages, pushing up prices on the 2020 wines and further reducing already limited availability. Consequently, Spain and South Africa are receiving increased buyer interest. Spain – with a wine stock recently estimated at 75.33 million hectolitres – is globally competitive on all bulk wines and, for European buyers, particularly so on generics. South Africa can offer good availability on 2020 wines at an excellent price/quality ratio, while its vintage 2021 is running smoothly following excellent growing conditions without weather extremes. Looking ahead to Spain’s harvest this year, a snowy January – 50% more precipitation than in a normal year – bodes well for groundwater reserves. California, meanwhile, has been e

10

As we enter the second month of 2021 the global bulk wine market can be characterised by being uncharacterizable: each producer country is currently contesting with its own unique cocktail of domestic and internationally-derived factors so that any sweeping statement about the global supply-demand balance would be suspect to say the least. Take the Southern Hemisphere: Argentina (+26.7% on 2019), Chile (-2%) and Australia (+0.5%) go into their 2021 harvests having experienced, given the pandemic, an impressive 2020 for their respective total wine export volumes. While this should mean tighter supply, in Argentina the supply tightness on varietals is mainly due to supplier speculation that prices will be higher later on (price increases that may be offset to the international buyer by the peso’s continuing devaluation); in Chile, unprecedented rainfall at the end of January has led to concern about 2021 vintage quality, so that many wineries are putting their sales on hold;

10