Another month of calm

November typically marks the end of a new harvest and the middle of our busiest sales quarter. October’s government shutdown created unbelievable market uncertainty. But with the system back up and Thanksgiving almost normal, stability returned rather than the predicted surges or collapses by pundits from both sides. Still, questions remain about the future of our economic recovery prospects. For now, it is a reprieve, allowing us to regroup for the new year.

Market dynamics

The delayed reports from Commerce and the Bureau of Labor Statistics have started to trickle in, bringing some key takeaways:

- Unemployment is holding at 3.8%.

- Inflation easing to 2.3% YoY.

- Consumer spending down ~2% from Q3, but no hint of a cliff.

As we close out the year and look to 2026, the focus will be on staying agile in both supply planning and capturing winery sales and marketing opportunities. The key trends persist: Steady demand, no major swings, and a growing gap between spenders and cautious households. Next year’s success will depend on how quickly you read market dynamics and adjust. Who you target and how the market recovers will shape the effectiveness of your strategy.

Deloitte projects 3.5% growth in holiday spending. High-income households will spend 7% more, while lower-income households plan to spend 4% less. Lower-income households are turning to value products, while premium segments stay steady. Brands are dividing their manufacturing and marketing to address both groups.

Steady-going operationally

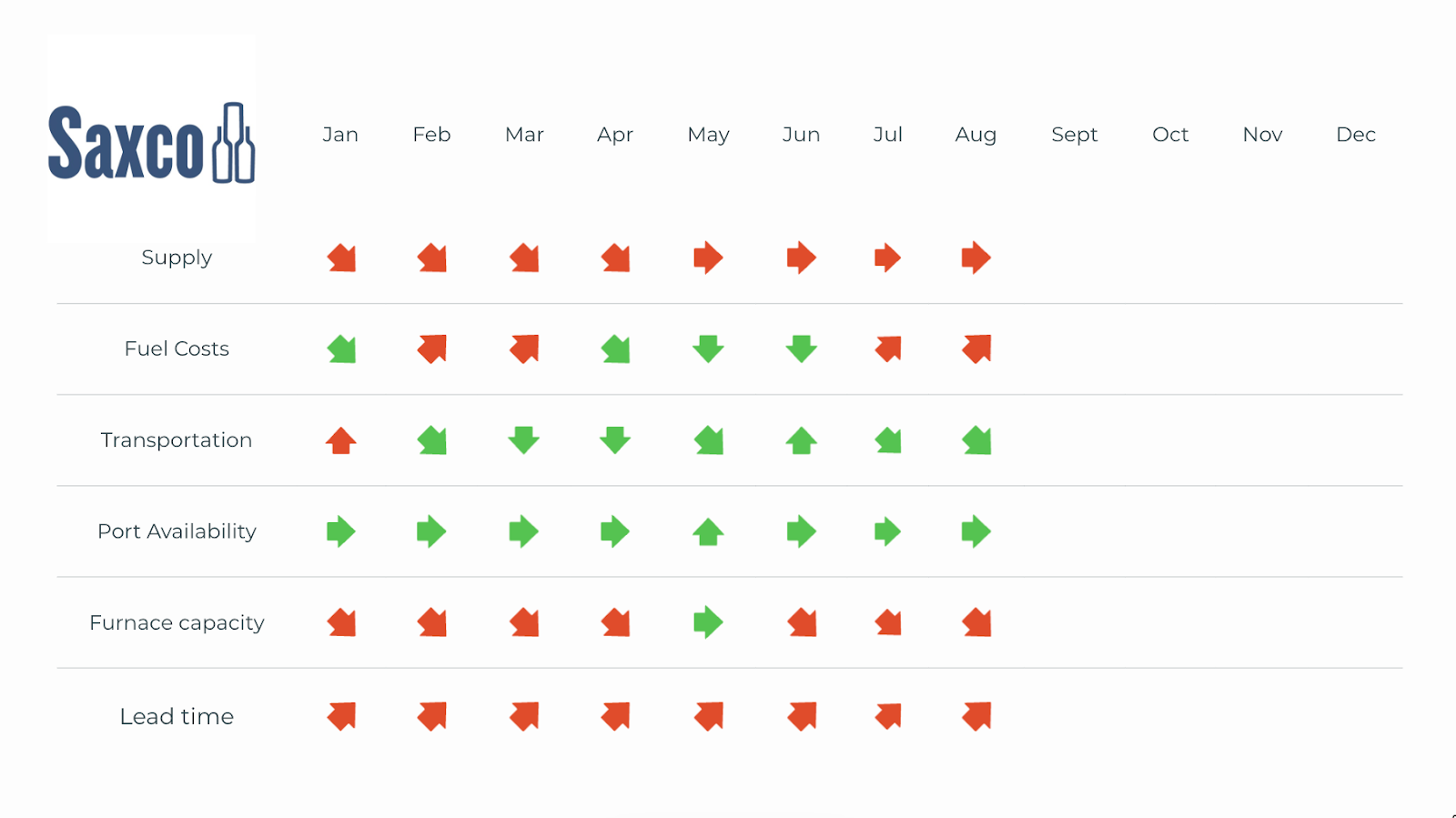

Packaging material deliveries for glass, cans, and closures in November were consistent, meeting the expected lead times without any notable delays or disruptions. Product quality and availability remained stable across all packaging types. Overseas freight costs for glass, cans, and closures eased slightly to $5,800 per container in November, down from $6,200 in October. While this is still above the roughly $4,500 level seen earlier in the year, there were no additional shipping bottlenecks or material shortages affecting packaging supply.

On the operational front, production trends held steady as well. Glass furnaces kept a steady pace in November.

In transportation, trends stayed similar to last month. Diesel sat at $3.42 a gallon, rail hit 94% on-time, ports stayed quiet, and trucking maintained usual booking windows. After the volatility of the last few years, these predictable patterns make that chaos feel distant.

The big date on the calendar is December 15th, when the anti-dumping and countervailing duty rulings finally land. Everyone is watching, but no one will be shocked by whatever the final judgment is. As year-end approaches, our main focus is the 2026 outlook.

Bottled Tidbits – The whole glass Christmas ornament thing actually started because of a challenging nut harvest. Go back in time to Lauscha, Germany, 1847, when a drought wiped out the nut harvest, which sounds small until you realize people literally hung nuts and fruits on their Christmas trees. No nuts, no ornaments, no holiday cheer.

The local glassblowers, already scrambling for side income, had to improvise. One of them, Hans Greiner, basically said, “If nature won’t give us nuts, I’ll just make them myself,” and started blowing glass versions. That simple workaround became the first generation of glass ornaments – better-looking and far more durable than the real thing.

Fast forward to 1880: Frank Winfield Woolworth is on a buying trip, sees these glass ornaments, and basically thinks: “No way Americans pay for this stuff”. He buys $25 worth just to try them out. They sell out in two days. Ten years later, he’s importing $800 million of glass ornaments annually. And Lauscha? It had turned into a full-on ornament powerhouse; 5,000 glassblowers making almost every Christmas ornament on Earth.

Here’s the most interesting part: The methods for making the ornaments became a nexus of innovation, pushing the entire glass industry forward. The silvering technique developed to make ornaments shine proved crucial for early vacuum bottles. And Max Eckardt’s machine from 1908 that crimped ornament caps? Bottle manufacturers took that idea and turned it into automated capping lines. Even the flashy metallic coatings you see on wine bottles today trace back to formulas created for Christmas baubles.

So this small German town, reacting to a poor fruit-and-nut harvest, ended up inventing much of the glass industry. It is a reminder that big leaps often come from refusing to accept, “That’s just how it is this year.” A useful perspective as we face tough headwinds.

Saxco, a leading provider of packaging solutions to the wine, spirits, beer and beverage industries, is pleased to announce a strategic partnership with Revino, a pioneer in reusable wine bottle systems, to deliver sustainable glass packaging choices for wine producers throughout the United States. The collaboration underscores both companies’ commitment to environmental responsibility and innovation within the wine industry.

Saxco has been at the precipice of innovative packaging solutions since its inception over 90 years ago. Continuing in its legacy, Saxco is now an official distributor partner of Revino’s acclaimed reusable wine bottles. The company has seen broad adoption with more than 100 winery partners and over one million bottles in circulation. Revino’s platform simplifies adoption of proven reuse models, helping wineries significantly reduce their environmental footprint without sacrificing brand integrity. Working with Saxco provides wineries with the benefits of logistical planning, redundancy of supply and hands-on packaging support from dedicated experts.

Packaging is the most carbon-taxing element of the winemaking process. Revino's returnable and reusable glass bottles provide up to 85% emissions reductions compared to standard single-use bottles, and are carbon neutral after three reuses, while suitable for up to 50 reuses.

These glass bottles provide wineries with meaningful cost savings, thanks to tariff-free manufacturing in the United States and their ability to be sanitized and reused. They reduce landfill waste while meeting increasing industry demand and regulatory requirements like Extended Producer Responsibility legislation. By adopting these practices, Saxco helps wineries participate in the circular glass economy, build operational resilience, and distinguish their brand. These sustainability commitments not only achieve environmental and financial goals but also appeal strongly to younger consumers, who prefer eco-friendly brands and are driving market trends toward transparency and responsible business practices.

"The partnership between Saxco and Revino reinforces our commitment to delivering sophisticated, sustainable packaging options to our wine customers," said Stephanie Ramczyk, Vice President, Wine Division at Saxco. "We’re thrilled to offer reusable wine bottles that align with their brand objectives and sustainability goals."

Adam Rack, Co-founder at Revino, added, "Partnering with Saxco allows us to expand the availability of circular packaging solutions to producers of every scale. Together, we are advancing the future of wine packaging with systems that prioritize sustainability without compromising on artisan quality."

As modern consumers increasingly seek eco-friendly packaging, Revino’s certified B Corporation status—combined with Saxco’s commitment to accessible, high-quality sustainable packaging—demonstrates both companies’ dedication to innovation and responsible business practices.

A pause in the fever dream of instability

October arrived not with fanfare but with something rarer: Quiet. After a year of collective anticipation for more and more problems, what occurred was a respite. The tariffs are stalled, and the early indications from the Supreme Court suggest they are still in flux and will be a topic for discussion on a future date. Fuel costs have stabilized, as have ocean freight rates.

There is a peculiar quality to this pause. It is that in-between moment that makes it hard to understand if wineries should keep their guard up or, finally, tentatively lower their shoulders.

The glass half empty, half full

The supply chain in October was like a strange dance. Everything remained unchanged – neither improving dramatically nor deteriorating. Just... holding.

Diesel slipped from $3.748 to $3.679 per gallon, a decline so modest it barely registers as movement. But after months of upward pressure, even sideways feels like progress. Ocean rates hit bottom not from efficiency gains, but from demand that has gone soft. The ports are clear – no congestion, no drama – but there is an unsettling absence of urgency in the quiet.

And the furnaces? Still the bottleneck. Still, the constraint that defines everyone else’s tempo. Lead times stretch into 2026 like a horizon that keeps receding.

The tariff plot twist

Then came the surprise nobody saw coming. After months of escalation rhetoric, Washington and Beijing chose détente over disaster. The fentanyl tariff has been reduced from 20% to 10%. The threatened November escalation to 34%? Canceled. Both sides agreed to a 12-month ceasefire – not a peace agreement, but at least a cessation of hostilities.

China reciprocated: Counter-tariffs were suspended, promises of agricultural purchases were made, and rare earth exports continued.

For glass and packaging, this translates to something precious: Predictability. No sudden cost shocks. No scrambling to recalculate pricing models. Just a few months of knowing what the rules are and finding peace in the predictability.

The market mood

There is a psychological aspect to October that numbers alone cannot capture. After months of crisis management, stability feels almost suspicious. Buyers who have been conditioned to expect the worst are slowly and cautiously starting to plan beyond next quarter.

The smart money is already moving and securing furnace time through Q2, locking in rates before the inevitable rebound, converting uncertainty into strategy. They understand that in a market built on lead times measured in seasons, predictability is currency.

There’s an old glassblower’s saying: “The best time to shape glass is when it’s neither too hot nor too cold – but in that precise moment when it’s willing to bend without breaking.” We recommend using this quiet time to really leverage the market stability for better planning and purchasing.

Here’s to keeping the glass half full.

Bottled Tidbits - The Venetian glass monopoly and the Prison Island of Murano

In 1291, Venice relocated all its glassmakers to the island of Murano under the pretence of fire prevention. The true motive was industrial security – Venice had perfected “cristallo,” the world’s first truly clear glass, and paper-thin goblets that could twist like sugar.

Murano’s glassmakers lived like aristocrats. They gained immense wealth and were celebrated. Often, they were granted noble titles. However, their privilege was a gilded cage, and it came with a catch: No one was allowed to leave the island. Any glassmaker caught trying to share Venice’s secrets abroad risked a quiet death at the hands of the Venetian agents, and glass making moved from being a trade to a state secret.

The strategy proved remarkably effective. For 200 years, Venice controlled the European luxury glass market through this combination of incentive and intimidation. No other region could match Venetian clarity, thinness, or decorative techniques.

The monopoly was broken in the 1670s when several glassmakers successfully escaped to Vienna and London. They took with them centuries of accumulated knowledge. Within a generation, these defectors had established competing glass centers that not only matched Venetian quality but also began developing their own innovations, including English lead crystal and Bohemian potash glass. Venice’s dominance, which was maintained by years of secrecy rather than innovation, could not survive the spread of its carefully guarded techniques.

This month: Soft seas, more questions, and a consumer that’s anxious and cautious about tomorrow.

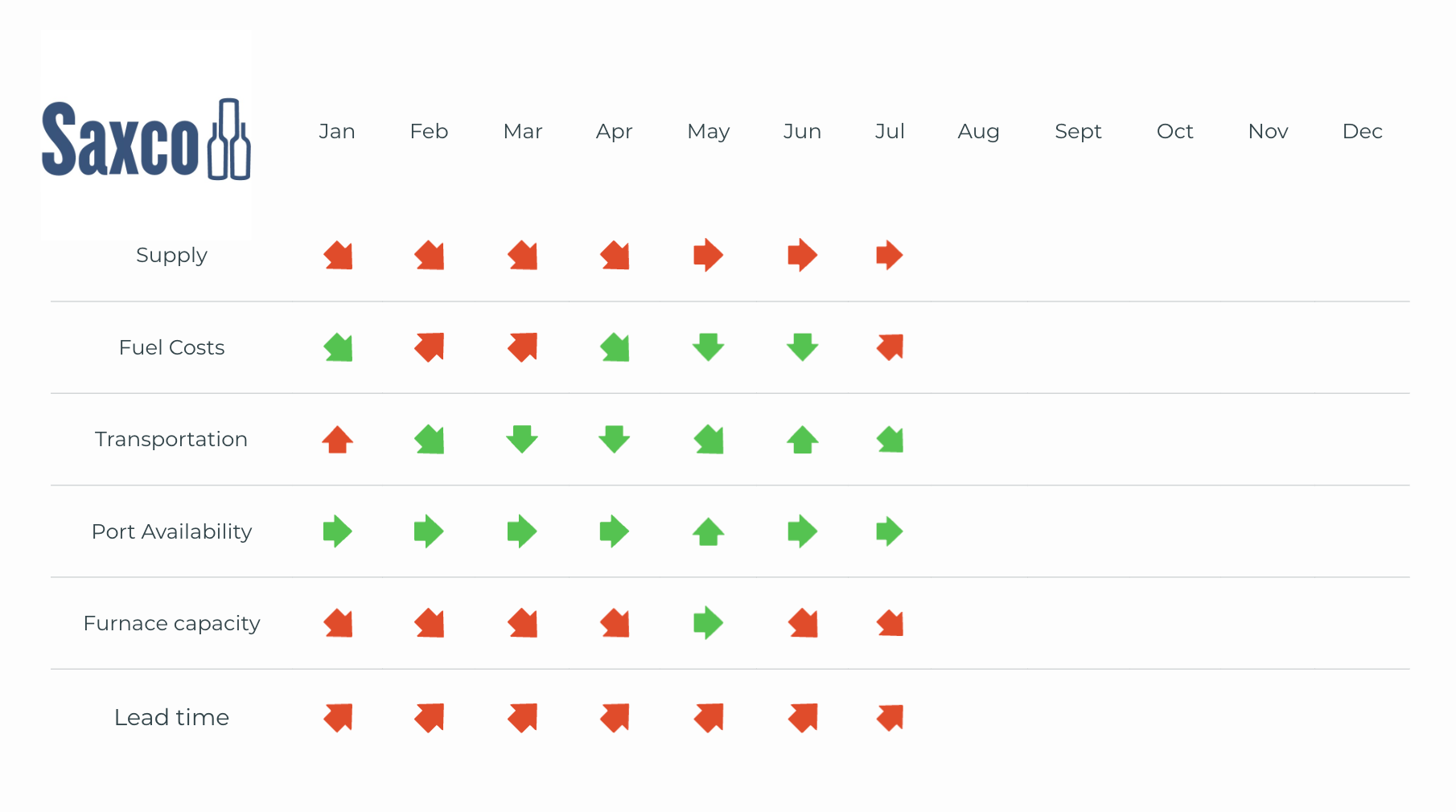

October’s here, and the supply chain feels eerily quiet. Not calm exactly – just slow. There is movement, but it’s more drift than direction. Freight rates are down, not because we have gotten more efficient, but because demand is low. Fuel is holding steady, but only because the broader economy seems reluctant to surge. There are no logjams at the ports, yet there is not much urgency, either.

Glass remains tight. Lead times are still creeping. And while retail shelves are being reset for the holiday sprint, the pace feels tentative. Brands are pushing forward, but many are doing so with a wary eye on cost, conversion, and the uncertain mood of the American shopper.

The story of October is about the tension between the inertia of supply and the jitteriness of demand. Between short-term calm and long-term concern.

Market overview

Fuel costs rose imperceptibly from $3.744 per gallon in August to $3.748 in September – barely a twitch on the needle, but still directionally up. More importantly, they have held within a narrow $3.70-$3.75 band for nearly a quarter, offering rare predictability in an otherwise jumpy economic landscape.

Ocean freight, on the other hand, continues to slide. Spot rates are now at their lowest level of the year, with demand falling below expectations from early summer. For some importers, this is a gift: Cheaper access, more expansive windows, fewer bottlenecks. But for others, especially those who bank on consistent movement, this softness is unsettling.

Port availability remains stable. No notable congestion. No major labor flare-ups. No climate shocks. It’s a rare pocket of neutrality in a system otherwise full of ifs and maybes.

Furnace capacity, however, remains a pressure point. The O-I Portland closure continues to cast a long shadow over domestic production. While the headlines have quieted, the knock-on effects persist – particularly for those relying on premium glass formats or just-in-time delivery windows.

Lead times are still stretched. Not wildly – but just enough to keep everyone on edge. There’s no slack in the system, no real room to play catch-up. Everything still takes more foresight than feels comfortable.

The consumer hesitates

Meanwhile, the consumer is still pulling back. Deloitte’s latest tracker has just landed, and the story remains unchanged. It’s not a precipitous drop, it’s just more erosion – a slow, quiet fade in confidence that keeps dragging on. Lower- and middle-income households are pulling back, especially in categories perceived as discretionary. Alcohol, specialty foods, and small indulgences are facing increased scrutiny, while essentials, promotions, and private-label goods are experiencing renewed strength.

There is also a psychological undercurrent: Shoppers aren’t just worried about now, but also uncertain about what’s next. Will tariffs drive prices up? Will Q1 bring layoffs or raises? Will a deal today look foolish tomorrow? These questions are not just background noise: They’re shaping cart sizes and channel choices in real time.

Retailers are responding by hedging their bets. Some are trimming holiday orders. Others are shifting toward value SKUs. Across the board, the expectation is that promotions will need to be both earlier and deeper to drive volume.

All of this is unfolding amid ongoing discussions about potential new tariffs on imported consumer goods and packaging materials. While the situation remains fluid, recent analyses suggest that the policy landscape could lead to some cost adjustments and operational pressures across retail and logistics. However, many industry leaders are already taking proactive steps to manage potential impacts through supply diversification, domestic sourcing, and strategic inventory planning. Whether or not the proposed measures move forward, the conversation is prompting thoughtful preparation rather than panic.

We get it, bottling season is chaotic, and hock bottles aren't top of mind. Avoid the last minute scramble and get your orders placed today. We have a variety of options to fit every budget. Whether you want to prioritize sustainability, domestic versus import, or even a custom mold - we've got you covered.

Reach out today to get in touch with our team of product experts. Reach out today to get in touch with our team of product experts.

The packaging supply chain is sending mixed signals this month – not quite cause for alarm, but enough yellow lights to keep procurement teams on their toes.

Let’s start with the good news: fuel costs edged down from July's $3.779 to $3.744 per gallon in August. But before we celebrate, some context is needed. At $3.74+, we're still hovering near the year’s second-highest diesel levels. Think of it as taking your foot slightly off the accelerator while still speeding – technically slowing down, but hardly cruising speed. Fuel remains a critical watch point as we head into Q4 planning cycles.

Transportation continues to be our bright spot. For the second straight month, we're seeing no peak season surcharges – a welcome relief that’s providing both cost predictability and operational flexibility at a time when the industry needs both.

Port operations remain stable with no meaningful congestion on key inbound lanes. The anticipated summer import surge never materialized into the bottlenecks many feared, keeping goods flowing smoothly through our major gateways.

The glass situation, however, tells a different story. The OI Portland closure continues to cast a long shadow over domestic production capacity. With no new furnaces coming online to compensate, we are seeing increasingly concentrated demand pressure on remaining facilities, particularly in California and the Upper Midwest. This structural capacity gap is not going away anytime soon.

Lead times crept up again – a trend that’s becoming concerning as we approach harvest season and holiday production windows. It feels like the days of JIT (Just-In-Time) inventory are a fever dream of the past and are not clever ways to operate, definitely in today’s environment.

Consumer sentiment: A study in contradictions

Deloitte’s latest State of the US Consumer report reveals a fascinating paradox. American consumers are simultaneously anxious about their finances and determined to maintain their lifestyle – particularly when it comes to experiences and affordable luxuries. They’re tightening belts with one hand while reaching for premium products with the other.

For packaging strategists, this schizophrenic spending pattern creates the need for a newfound agility. It’s hard to predict demand when it can easily pivot sharply, especially for packaging that serves premium segments or special occasions. The consumer who skips the restaurant meal might still splurge on the premium bottle for home consumption.

The Bottom Line

We are operating in a market that looks stable on the surface – but is quietly fragile underneath. Fuel prices remain stubbornly high, domestic glass capacity is under pressure, and shifting consumer behavior means surprises are always on the table.

The supply environment may read as “narrowly neutral,” but that equilibrium is precarious. The smartest operators are building in flexibility now – because in a market like this, neutral can turn negative faster than you can say “supply chain disruption.”

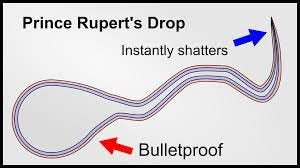

Bottled Tidbits – Glass that can stop a bullet but shatters at a touch

In the strange world of glass, few phenomena are as baffling, or as beautiful, as Prince Rupert’s Drops. These tadpole-shaped beads of glass have puzzled scientists for over 400 years. Strike the bulbous head with a hammer or even a bullet, and they hold firm and can withstand forces up to 664,300 Newtons (nearly 67,740 kilograms). But tap the fragile tail with your fingertip, and the entire structure explodes into dust at almost the speed of sound.

They are formed by dripping molten glass into cold water. The outer shell cools rapidly and locks in extreme compressive forces – up to 700 megapascals, nearly 7,000 times atmospheric pressure. Meanwhile, the core remains under intense tension. This opposing force profile makes the exterior strong as steel, but the interior a ticking time bomb. Snap the tail, and cracks race inward at 1,900 meters per second (4,200+ mph), obliterating the drop in a violent instant.

Prince Rupert of the Rhine brought them to England’s King Charles II in 1660 as a scientific novelty; these “Dutch tears” would remain a mystery for centuries. It was not until 2017 that modern imaging revealed the actual mechanics behind their paradoxical strength – and fragility.

Prince Rupert’s gift to the king wasn’t just a conversation starter – it was accidentally the key to modern tempered glass. Those same internal stresses that made courtiers gasp in amazement now protect every skyscraper window and phone screen on the planet. It’s always amazing to find that the origins of some of the greatest modern materials were just accidental discoveries.

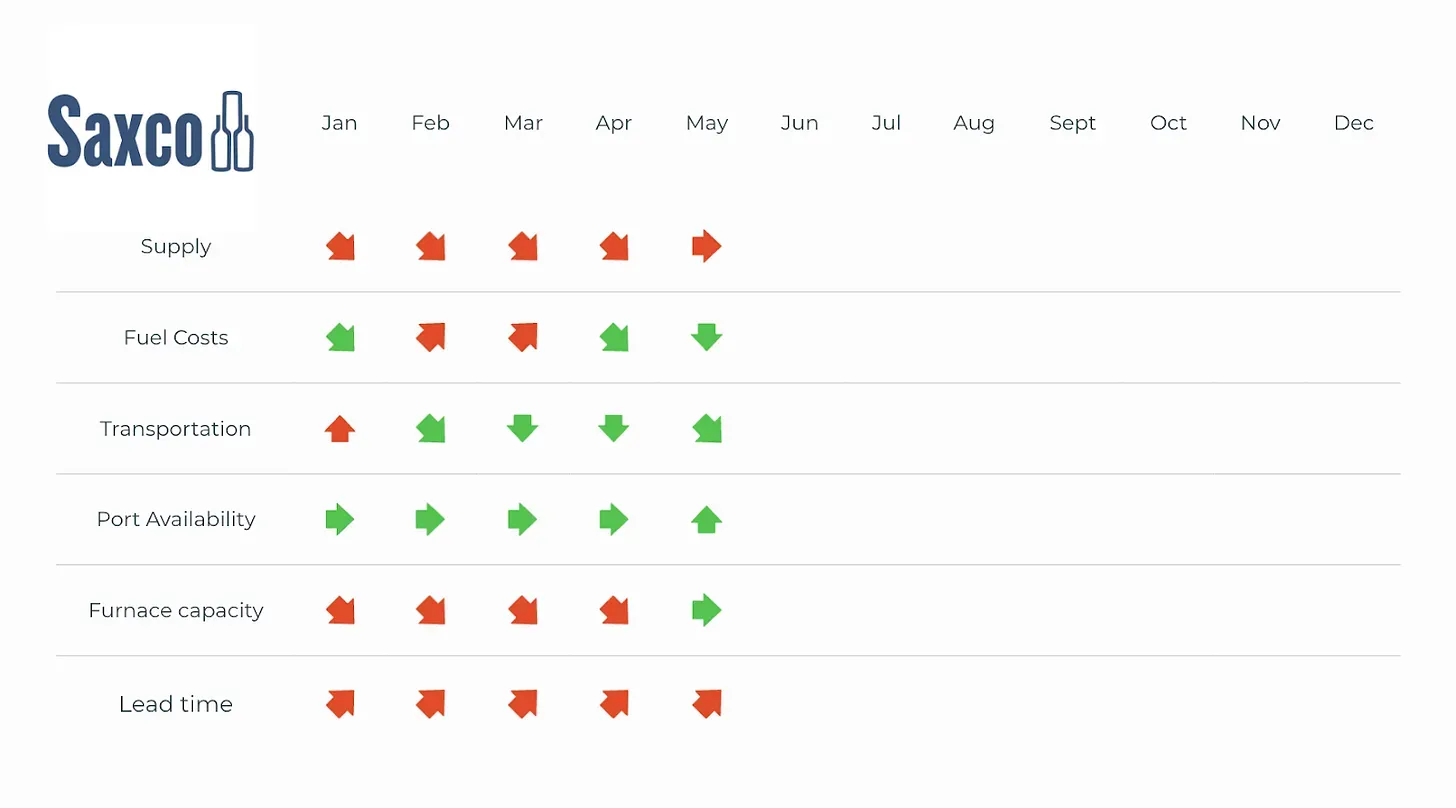

July's supply chain landscape feels deceptively calm, but the undercurrents are shifting. Fuel costs ticked upward again – $3.599 to $3.779 per gallon – putting quiet pressure on logistics, even as transportation costs eased with the surprising disappearance of peak season surcharges. That dip is a welcome but likely temporary reprieve.

On the production side, capacity continues to tighten: OI’s Portland plant has officially closed, and two additional furnaces are scheduled to go offline, which continues to raise concerns about domestic supply heading into the back half of the year. Lead times have not budged from June’s elevated levels, but with fewer furnaces online, we are likely to see that stress compound by fall. Ports remain neutral, and overall supply feels steady – but for now, it is a still surface over increasingly strained infrastructure.

Tariff watch: The rules are changing

The new US tariff rates announced on July 31 mark a significant shift in the trade wind –particularly for glass and wine. EU imports are now subject to a 15% tariff on standard wine bottle sizes (375ml, 750ml, and 1L), a move that will reshape sourcing math for many in our industry. The new rate took hold August 7, but the old rates apply for goods that meet certain “on the water” criteria before August 7 and are entered for consumption before October 5. Still, any attempt to sidestep these costs through transshipment could trigger a brutal 40% penalty tariff, plus potential fines or penalties – no small risk for those trying to outmaneuver the system.

The aggregate US IEEPA tariffs on Indian glass increased to 25% on August 7 and will rise to 50% on August 27, while the aggregate US IEEPA tariffs on Chinese glass are still scheduled to increase from 30% to 54% on August 12 – unless a diplomatic off-ramp appears. In Canada, fentanyl-linked tariffs rose from 25% to 35% this month, though USMCA-origin goods remain safe.

Taken together, this constellation of tariff shifts signals a more complex and costly global market – especially for smaller-format bottles and price-sensitive products. Reports from the EU and New Zealand warn that boutique exporters may be among the hardest hit. For importers and bottlers in the US, strategic recalibration is no longer optional – it is now table stakes.

Consumer pulse: Value, redefined

Consumer behavior is shifting in ways that matter for packaging decisions. Deloitte’s latest numbers show over half of consumers have switched brands recently, but not necessarily to save money – they are chasing better value. There is a difference, and it shows up in purchase patterns. Nearly 40% plan to treat themselves to something small but meaningful this quarter, which keeps premium consumables in play if they justify the spend.

This nuance is especially relevant in categories like premium wine and spirits. Over half of consumers say they have recently switched brands to find better value. Not better pricing – better value. That could mean a more beautiful bottle, a more compelling backstory, or simply a product that feels like a reward. As mentioned, nearly 40% say they plan to indulge in something small but meaningful this quarter, which means there is still oxygen for premium formats – if they speak to the moment.

For glass customers, this is not a race to the bottom. It is an invitation to differentiate. In a value-driven world, quality, story, and detail still win.

Bottled Tidbits – Daylight robbery: The tax that dimmed the world

Before the 17th century, windows were not a structural standard – they were a status symbol. Glass was so rare that when Britain needed to raise funds in 1696, Parliament did not tax income or land. Instead, they taxed windows. It is a fact: homeowners were charged based on the number of glass panes they had. The result? A generation of buildings with bricked-up windows is still visible across parts of Europe today. It was known as a “tax on light and air,” and it is where we get the phrase "daylight robbery”.

Though repealed in 1851, the damage lingered: historical records show glass production between 1810 and 1851 was essentially flat, despite a housing boom. Only with mass manufacturing did both windows and bottles become widespread. Glass was not always everyday. Once upon a time, it was the dividing line between those who could look out and those who could not afford to.

Packaging supply stable, but uneasy

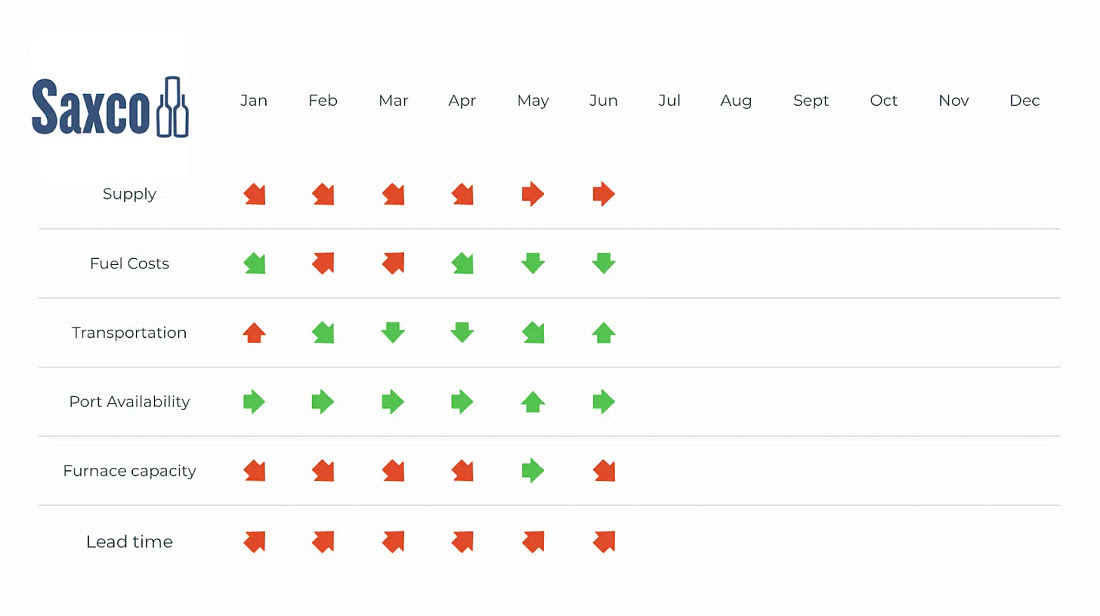

While June ushered in a more stable rhythm after May’s tariff-driven frenzy, underlying uncertainty continues to shape planning, procurement, and pricing across the packaging and logistics landscape.

Supply remains steady across most categories, but stability doesn’t mean simplicity. US glass manufacturers, in particular, are contending with a mismatch between output and demand. Inventories have piled up amid sluggish ordering, especially from wine producers still reeling from compressed consumer spending and slowing DTC velocity. With tanks and warehouses more full than empty, some domestic furnaces are now eyeing Q3/Q4 production pauses as a measure to rebalance.

After a brief reprieve in May, diesel prices rose again in June, increasing from $3.499 to $3.599 per gallon, a continued reflection of the volatile energy market. According to the latest Deloitte economic outlook, while core inflation is showing signs of moderation, energy prices remain sensitive to global geopolitical tension and supply disruptions – factors that could ripple into transport costs if sustained.

A welcome shift: Ocean freight rates are finally softening. The temporary spike in May – triggered mainly by the rush to export from China after the Trump administration’s tariff adjustment announcement – has now normalized. With much of that panic-driven demand behind us and Peak Season Surcharges dropping off for July, space is opening up and rate pressure is easing. Expect less turbulence and better booking windows through mid-summer, especially for trans-Pacific lanes.

No major disruptions at key US ports this month. Container flow has steadied, and with fewer surcharges in play and less congestion at origin points in Asia, downstream bottlenecks are easing. However, West Coast labor agreements and geopolitical flashpoints remain lurking variables to monitor.

Domestic furnace capacity remains technically stable, but looming stress is on the horizon. As noted, with US manufacturers holding higher-than-normal inventory and facing muted forward demand, the sector may reduce operating throughput later this year. Manufacturer inventory recalibrations could impact availability and price negotiations for Q1 2026, especially for custom molds or specialty projects.

Lead times remain elevated across glass and closures, with no significant change from May. Extended replenishment cycles are being driven by a combination of slower burn rates, cautious forward ordering, and lingering backlog from earlier transportation disruptions.

While last month’s flurry stemmed from the announcement of lower tariffs on Chinese glass, that has since cooled, but uncertainty remains. The tariffs remain in place, and the administration has signaled that the policy could shift again in the future. Wineries should continue to hedge with a balance of domestic and international sourcing, and closely monitor the ever-changing tariff policies.

According to Deloitte’s June 2025 economic forecast, the broader US economy continues its “soft landing” trajectory – growth without recession, but not without friction. Consumer sentiment has improved slightly, but spending remains cautious, particularly in categories tied to discretionary lifestyle purchases (like wine). For suppliers, this means maintaining agility and avoiding overextension.

The worst of the tariff-related chaos may be behind us, but we are not yet in calm waters. Pricing, transportation, and inventory planning all require careful attention through the remainder of summer.

Bottled Tidbits - The origin of the ‘punt’ in a bottle remains a topic of debate. Some say it was used to collect sediment in the days before wine filtration became a common practice. Others argue it helped glassblowers shape the bottle or added strength for sparkling wines under pressure. There’s even speculation that punts made bottles easier to stack – or made pouring feel more ceremonial. But in reality, punts originated from the practical needs from the days when bottles were only glass-blown. When bottles were hand-formed, the base seam was pushed inward to ensure the bottle could stand upright and to eliminate the sharp glass tip that formed during the blowing process – a simple solution that became a lasting design feature.

Today, the punt persists primarily as a tradition and marketing tool. A deeper punt still often signals a more “premium” bottle. The practical need evolved from form to folklore until the punt became a visual shorthand for luxury and now has become a packaging cue, subtly signaling quality and prestige, regardless of what’s actually inside the bottle.

As we move into the summer shipping season, the overall supply chain remains relatively stable – though a few indicators are beginning to shift. Here’s what we’re seeing across the key areas impacting glass packaging and logistics.

Glass supply is holding steady, with no significant disruptions reported across domestic or international sources. Availability has remained neutral for several months now, though specific bottle types and molds still see some intermittent constraints. That said, there is a growing awareness in the industry of potential pressure on furnace capacity later this year. Conversations are underway about potential closures in Q4, which could result in tighter availability in early 2026 if demand remains stable or increases.

Diesel prices edged downward in May, offering slight relief for overland freight. The national average fell from $3.567 per gallon in April to $3.499 in May. This small but welcome drop comes at a time when other transportation costs are trending in the opposite direction.

Ocean freight, particularly from Asia to the US, is climbing quickly. Rates on both West and East Coast lanes have risen sharply since last month. Peak Season Surcharges (PSS) went into effect on June 1, with another increase already scheduled for mid-month on June 15. This adds new cost layers to international shipments as import activity ramps up ahead of Q3 programs.

Despite this, US port availability remains neutral. Terminals are functioning within expected capacity ranges, and there are no significant bottlenecks at the time of this writing. Still, any surge in freight driven by the PSS or forward-buying in anticipation of future tariffs could strain throughput later in the quarter.

Lead times continue to trend upward, particularly for custom molds and anything involving multi-step international sourcing. While the situation hasn’t worsened since May, extended planning windows remain necessary across most categories.

In the background, there’s growing attention on trade policy signals -particularly around the Trump campaign’s proposal for new tariffs on steel and aluminum. While these policies haven’t been enacted, the potential for sweeping import duties has already triggered concern within the industrial packaging sector. Glass may not be directly targeted. Still, tariff-related input costs and manufacturing equipment pricing could be affected, especially if the policy environment shifts again.

For more detail, the Council on Foreign Relations has published a helpful summary: Trump’s New Aluminum and Steel Tariffs Explained.

Bottled Tidbits - According to ancient legend, the first glass was made by accident. Around 3,500 BCE, Phoenician merchants shipwrecked on the Levantine coast built campfires on the beach using blocks of natron (a type of mineral salt) from their cargo. As the fire burned, the heat fused the natron with sand, forming puddles of a strange, glassy substance. This early proto-glass wasn’t yet what we’d call bottle-grade - more glaze than a vessel - but it kicked off centuries of experimentation.

From those fiery beginnings, glassmaking evolved across Egypt, Mesopotamia, and eventually Rome, where techniques such as blowing and molding transformed glass into a functional - and ultimately indispensable - material. A happy accident became a cornerstone of civilization.

In recent years, US trade policy developments – including broad tariffs and anti-dumping/countervailing duties – have disrupted global supply chains and increased costs across multiple industries. The wine and spirits sector, in particular, continues to experience the ripple effects of trade tensions involving key packaging sources such as China, Mexico, and Canada, along with ongoing tariffs on aluminum and steel.

On April 2, 2025, President Trump invoked emergency trade powers under the International Emergency Economic Powers Act (IEEPA), imposing a 10% “baseline” IEEPA tariff on most imported products from most countries, effective April 5. Higher tariff rates on imports from 57 countries were temporarily suspended for all but China, providing a 90-day reprieve. Meanwhile, China was subjected to 125% IEEPA reciprocal tariffs plus 20% IEEPA “fentanyl” tariffs, as well as any other applicable tariffs, such as the 25% China Section 301 tariffs initially imposed during President Trump’s first term.

On May 12, the US and China agreed to a 90-day reduction in tariffs, effective May 14. This will reportedly result in a reduction to U.S. IEEPA reciprocal tariffs on Chinese goods from 125% to 10% but not affect the 20% IEEPA fentanyl tariffs or other applicable duties. China's tariffs on US imports will reportedly fall from 125% to 10%, also effective for 90 days.

Despite this short-term tariff relief, significant US trade restrictions remain in effect, including alternative 25% duties on steel, aluminum, and automobiles, as well as alternative 25% tariffs on Canadian and Mexican products that do not meet the origin requirements under the US-Mexico-Canada Agreement, or USMCA.

While financial markets responded positively to the immediate easing of tariffs – with major indices seeing temporary gains – long-term business confidence remains fragile amid ongoing uncertainty. Federal Reserve Chair Jerome Powell has cautioned about potential stagflation should trade instability persist. Additionally, JP Morgan estimates sustained tariffs could negatively impact global GDP by up to 1%.

Tariff implications for the wine industry

Given this persistent volatility, the wine and spirits industry remains cautious, proactively recalibrating supply strategies. Businesses are encouraged to carefully evaluate their exposure to supply disruptions – especially from China, Mexico, and Canada – and implement measures such as securing long-term contracts, maintaining safety stock, and identifying alternative supply channels in collaboration with their packaging partners.

The monthly changes across key channels are still fairly stable; however fuel costs are slightly down with US diesel lower from $3.585 in March to $3.567 in April. We anticipate increases starting in May as we approach the summer months and on the heels of some refinery closures and maintenance. We also see some port availability and lower transportation costs as a result of lowered imports from China.

Bottled Tidbits – For most of history, glass was a fragile instrument we drank from or looked through – whether it be a window, a set of reading glasses, or a television. It always needed some level of durability but did not require the everyday strength of clumsy humans using it for almost five hours a day. Then came the smartphone, and everything changed.

The moment we started putting glass in our pockets – expecting it to survive keys, curbs, and concrete – scientists had to rethink everything they knew about strength, flexibility, and resilience. And so began one of the most remarkable chapters in material science.

Enter Gorilla Glass, a sleek, nearly invisible armor forged by Corning. Designed to resist drops and scratches, its toughness is due not just to science but also to a stunning manufacturing process. Using a technique called fusion draw, molten glass flows like honey and forms whisper-thin sheets as it cools mid-air – a breathtaking balance of heat, gravity, and precision.

But then the glass plunges into a molten salt bath, heated to around 400°C to make the magic happen. This isn’t spa treatment – it’s ion exchange, where tiny sodium ions inside the glass are pushed out and replaced with bigger, brawnier potassium ions. The result? A layer of internal tension that gives the glass its almost supernatural strength.

And when you think the story can’t get more sci-fi, along comes AM-III – the world’s hardest glass. Scientists created it by crushing carbon fullerenes, then applying intense heat and pressure – 1,200°C and 25 gigapascals, to be exact – for twelve hours straight. Then they let it cool. The result? A clear, durable glass that can scratch a diamond.

This isn’t just about better phone screens – these breakthroughs open doors in solar energy, aerospace, and protective tech. What started with a cracked phone screen has turned into a quiet revolution – one in which everyday glass is becoming smarter, stronger, and almost indestructible. It also is almost as efficient as silicon to conduct electricity. So the next time you tap your screen or glance through a window, remember: you’re looking at centuries of invention – and a future that’s still being shaped, one atom at a time.