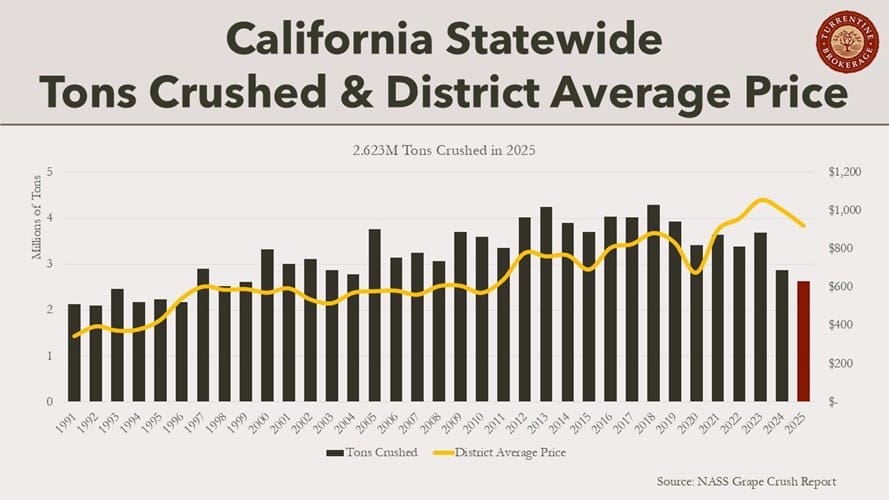

2.62: A Historic Reset

by Steve Fredricks

The release of the preliminary 2025 California Crush Report confirms an evolutionary shift in the state’s wine landscape. With the total crop recorded at 2.62 million tons, the industry has hit its lowest production level since 1999. This marks the second consecutive small harvest, resulting in a staggering one-million-ton decrease in tons harvested compared to just two years ago. For the consumer market, this translates to roughly 73 million fewer cases available between the 2023 and 2025 vintages, reflecting a deliberate, industry-wide effort to bring wine production back into balance with current demand.

The impact of this contraction was felt most acutely in California’s interior regions. While coastal areas saw a 51,000-ton decrease compared to 2024, the interior experienced a much sharper drop of 170,000 tons. This disparity highlights a significant trend: acreage is being removed from production at a higher rate in the interior as the growers and wineries adapt to soft demand for wines priced under $10. While the premium segments typical of the coast are also facing challenges, the interior is seeing a more rapid structural adjustment.

Despite the smallest Chardonnay crop since 1999, white grape tonnage exceeded red grape production in 2025 for the first time in three decades. This change was less about bearing acreage and more about making strategic decisions on what to harvest. The transition was mostly due to the steep reduction in red blenders crushed for production coupled with growing acres of Sauvignon Blanc and Pinot Grigio. The data suggests that wineries are prioritizing white varieties to align with consumer interest.

In This Issue

- Bulk Market 3

- Cabernet Sauvignon 4

- Chardonnay 4

- Sauvignon Blanc 5

- Pinot Noir 5

- Conclusion 5

- Market Opportunities 6

March 13, 2026 (Novato, CA) — Following the release of the Preliminary 2025 California Grape Crush Report, Turrentine Brokerage, the largest California grape and bulk wine brokerage company, has issued a market assessment characterizing the 2025 vintage as one of the most challenging for the wine industry since Prohibition.

According to the new state data, the total tons crushed came in at 2.62 million tons, a figure that is above initial projections and well above what was felt by the industry. This statewide volume is 8% below 2024 and 23% below the 5-year average. Total red wine production declined by 9% and white wine production declined by 6%. “The decrease in tons is still very positive news for the industry overall,” said Steve Fredricks, President at Turrentine Brokerage.

“The 2025 vintage highlights the industry’s directional shift of declining production and an overall restructure of the industry. 2025 represented continued challenges for growers and wineries that were strikingly apparent at harvest,” said Audra Cooper, Vice President

at Turrentine Brokerage. “Between a cooler growing season, reduced vineyard inputs, and multiple rain events which led to excessive late-season disease pressure and combined with soft demand, 2025’s challenges were relentless.”

Key Takeaways from 2025:

- A Correction in Volume: The 2025 crop is the lightest on record since 1999. This reduction is attributed not only to weather and acreage removals, but also a lack of grape demand, which left significant tonnage uncontracted and unharvested.

- Reduced Crop Value: The total 2025 crop value throughout California was down 16% from last year to $2.414 billion, and down 22% from the five-year average. Cabernet Sauvignon, Chardonnay, Pinot Noir, and Zinfandel declined more than $330 billion in total crop value from last year.

- Low Market Activity: Buying activity for grapes and bulk wine remained low statewide through the end of the season. Late-season activity was largely limited to opportunistic plays in the North Coast and Paso Robles for Cabernet Sauvignon, with minimal movement to replace grapes rejected due to disease pressure.

Industry Analysis & Outlook

The 2025 Grape Crush Report highlights a pivotal moment in the restructure of the California wine industry. Wineries planned to go light on this vintage, and it is estimated that 57,000 acres were removed with significantly more unharvested in 2025. This strategic decision,

combined with the seasonal challenges, has accelerated the market’s transition. The five-year average crop size from 2019 to 2023 was

3.6 million tons. The efforts to reduce crop size in 2025 has resulted in a decrease of 1 million tons from the five-year average, or the equivalent of 72 million cases.

While the industry is largely trending toward a decline in total production, Sauvignon Blanc increased 22,000 tons and Pinot Gris increased 8,000 tons from 2024. This is concerning with more acres coming into production on both varieties, and Sauvignon Blanc is being heavily discussed between nurseries and growers for additional plantings.

Following are the largest takeaways by region:

North Coast, Christian Klier

- “Tons crushed of Napa Valley Cabernet Sauvignon in 2025 were similar to 2024 due primarily to an increase in yield per acre, with the district average price decreasing modestly.”

- “District average prices throughout the North Coast are not representative of the spot market prices for new contracts for the second consecutive year. An example of district average price varying dramatically from spot market pricing is Sonoma County Chardonnay with the district average price of $2,370 while spot market prices were closer to $800 per ton.”

- “District average prices for Mendocino County Pinot Noir surpassed Sonoma County due to the lack of large volume end-of-season deals coupled with relatively high prices per ton in Anderson Valley.”

Central Coast, Eddie Urman

- “The 2025 yields per acre were substantially healthier than 2024, despite harvesting 10,700 fewer tons. Total Central Coast tons were not reflective of the unharvested volumes left behind by the soft market.”

- “Central Coast Cabernet Sauvignon production has dropped by 52,000 tons from 2023, reflecting a market contraction. However, District 8’s crop is up 13% year-over-year, thanks to better yields per acre and demand for Paso Robles grapes compared to neighboring regions.”

- “District 7 and 8 Sauvignon Blanc total tons crushed increased by 32% over 2024, which puts it in line with the monster crop of 2023; however, it is important to note that there were significant volumes of Sauvignon Blanc that went unharvested in 2025 creating a false since of how much supply has grown in the Central Coast.”

- “District 8 Cabernet Sauvignon sales value has declined 44% since 2023. More accurately highlighting the pressure growers have felt over the past few years compared to the 11% decrease in the district average pricing from 2024 to 2025.”

San Joaquin Valley, Mike Needham

- “Statewide tons crushed for French Colombard declined by more than 46,000 tons while Muscat of Alexandria was down more than 18,000 tons, reflecting the combination of soft demand and acreage removals, particularly in the South Valley.”

- “The Lodi Chardonnay crop was the smallest on record since 1998, coming in at 86,000 tons. 2025 marks the second year below 100,000 tons.”

- “California Zinfandel continues to see a dramatic decline in production, with only 51,400 tons crushed in Lodi (District 11). This region historically had always been above 100,000 tons prior to 2023.”

About Turrentine Brokerage

Turrentine Brokerage, founded in 1973, serves as trusted and strategic advisors to growers, wineries, and financiers and specializes in the strategic sourcing of wine grapes and bulk wine from the major growing areas across the globe. Working with thousands of wineries worldwide, and with over 2,000 growers, this experienced team has negotiated transactions between buyers and sellers valued at more than $3 billion over the past decade.

WHAT: The California Department of Food and Agriculture’s Preliminary Grape Crush Report for 2025 is a barometer for the wine and grape industry, containing prices and tons of wine grapes crushed. The Crush Report provides growers and wineries insight into the inventory position for the California wine business as a whole, and can influence market dynamics for the current bulk wine and grape markets as well as potential impacts at the consumer level.

WHAT: The California Department of Food and Agriculture’s Preliminary Grape Crush Report for 2025 is a barometer for the wine and grape industry, containing prices and tons of wine grapes crushed. The Crush Report provides growers and wineries insight into the inventory position for the California wine business as a whole, and can influence market dynamics for the current bulk wine and grape markets as well as potential impacts at the consumer level.

WHEN: CDFA is scheduled to release the Crush Report at 12:00PM PST on Friday, March 13th, 2026.ANALYSIS: A historically small crop coupled with below break-even spot market grape pricing compounds wine industry headwinds. For the second consecutive year, the California Crush Report will reflect a wine industry navigating a significant supply-and-demand imbalance. While actual tons harvested remained historically light across many regions in 2025, the primary driver of market instability is the sustained decline in consumer demand and a lingering oversupply from previous vintages. This surplus has pressured the average price per ton downward, with spot market pricing falling below break-even levels for many growers for the second or third year running, depending on region. Because agricultural lenders frequently utilize the Crush Report’s pricing data to determine valuations, these suppressed figures are expected to further restrict access to capital, intensifying the financial strain on an already fragile industry.

Turrentine Brokerage can help provide clarity to the Crush Report data summary. Our proprietary sales data provides real-time insights into the spot market, offering a more accurate picture of the balance of supply to demand than potentially misleading district averages. Furthermore, our detailed acreage calculations, combined with actual crush tonnage data, will provide valuable insight into vineyard removals by region and variety. This analysis can reveal significant shifts in supply and demand, ultimately impacting grape prices and, eventually, consumer costs.

WHO: With over 50 years of wine industry experience, Turrentine Brokerage, California’s largest wine grape and bulk wine brokerage company, has a team of trusted strategic advisors to wineries, growers and financiers.

Turrentine Brokerage will have its experienced team of grape and wine brokers and analysts available all-day Friday, March 13th, and throughout the following week for comments and questions.

Beyond the Peak of Excess

by Steve Fredricks

As we turned the calendars to 2026, the landscape felt familiar: excess inventories, a scarcity of buyers, and a relentless stream of negative headlines that keep the wine markets entrenched in a perception of "peak of excess." While it is true that some inventories remain swollen and activity in the bulk wine and grape markets is sluggish, significant actions (and reactions) to correct this oversupply have been underway behind the scenes for years. These actions are beginning to come to the forefront in the form of vineyard removals and, unfortunately, the closing of wineries and other associated businesses in the industry.

The combination of unsold tonnage and strategic vineyard removals has limited both recent crop sizes and reduced future supply potential. The 2024 crop, totaling 2.864 million tons, was the smallest in 20 years; 2025 is likely to be dramatically smaller. However, projecting actual tons crushed for 2025 is particularly challenging due to the high volume of uncontracted fruit, mothballed vineyards, quality rejections, and extensive acreage removals, leading to a wider range of forecasts than usual. Our grape brokers—with "boots on the ground" throughout the state—project the 2025 crop to fall between 2.0 and 2.4 million tons. This would mark potentially the smallest harvest since the mid-1990s.

Our projections for 470,000 bearing acres in 2025 were confirmed by the Land IQ survey in November. Out of necessity, we expect another 50,000 acres to be removed or mothballed in 2026 unless growers secure early contracts. With these additional removals, a 2026 crop size of roughly 2.75 million tons would be expected, assuming long-term average yields. However, with many vineyards recently mothballed or otherwise minimally farmed to reduce yields and costs, there could be considerably lower potential yields.

Though we may feel stuck in a period of excess, the results from difficult decisions made over the last two years to reduce inventory are continuing to work through the three-tier system. On the supply side, we are shifting away from oversupply, even if the spot bulk wine and grape markets have yet to fully realize or be impacted by it.

While this has been a painful but necessary correction, the large number of acres removed could swing the pendulum back towards shortage at some point in the next couple of years, particularly if consumer sales stabilize. Removals out of necessity compared to forward thinking strategy could lead to a turbulent transition, and the abundance of choice a buyer has had recently may dissipate. If significant removals continue to happen, and yields are smaller than historical averages this year, the 2026 crop could be a bellwether for all markets shifting further away from excess and towards shortage. As we move through the year, we will monitor and analyze bulk market supply and demand indicators as they can elicit data points of looming change. This issue of the Turrentine Market Update is centered more on the early bulk wine market as the grape markets were reviewed in early November.

- Bulk Market 3

- Cabernet Sauvignon 4

- Chardonnay 4

- Sauvignon Blanc 5

- Pinot Noir 5

- Conclusion 5

- Crop Contest 6

- Turrentine on the Road 6

Perfect Storm

by Steve Fredricks

We are nearing a wrap to harvest for one of the most difficult years for the wine industry since Prohibition. Grape and bulk wine buying activity at the end of the season continues to be generally low statewide, with only a few opportunistic plays in the North Coast and Paso Robles and very little activity to replace grapes unfortunately rejected in any region.

The 2025 vintage was a perfect storm that came to a head at harvest. Among the multitude of challenges this year were a cooler growing season, low vineyard inputs due to diminished prices, minimal grape demand leading to uncontracted fruit, and multiple rain events during harvest which increased disease pressure on grapes already struggling to reach minimum Brix. Statewide, there are still many tons on the vine with multiple rain events in the latter half of October essentially ending harvest for many growers. Despite these challenges, there are numerous reports of very good quality wines.

Projecting total tons crushed in 2025 will be particularly difficult due to the lack of accurate information on acres removed, unfarmed acres, and the number of acres unharvested. What is clear, however, is that wineries have planned to go light on the 2025 vintage due to conservative sales forecasting and financial limitations amid sliding consumer sales trends. It is also clear that the incredible challenges this year will result in what is likely to be the lightest crop on record since the mid-1990s and will be impactful in the future market transition from excess to balance.

- Forward Thinking Strategy

- Bulk Market

- Cabernet Sauvignon

- Chardonnay

- Sauvignon Blanc

- Pinot Grigio

- Pinot Noir

- Other Reds

- Crop Contest

- Turrentine on the Road

- Market Opportunities

Groundwork for Tomorrow Harvest & Bulk Update

by Steve Fredricks

The California wine industry remains at a stark disconnect between supply and demand. As a result, the supply side of the industry continues to undergo a significant, painful transformation to reduce supply and right size inventories by removing vineyards, closing wineries, liquidating wine, and reducing grape and bulk wine purchasing to meet the reduced consumer demand.

As we know, information in the wine industry has always been imperfect and delayed, whether this be incomplete sales data, slow-to-mature vineyards, or acreage removals of late. Despite the efforts from both wineries and growers to limit supply, market indicators like bulk wine and grape prices still point to the need for further supply reduction, but this could be tied to the aforementioned imperfect and delayed data. Unfortunately, while the wine industry is waiting to realize the full impact of this work and whether more needs to be done, finances at all levels of the industry are strained. This creates a challenging environment where conservative inventories are the safest strategy, causing wineries and growers to tackle immediate problems rather than strategically plan for the future.

At Turrentine Brokerage, we are committed to gathering comprehensive information and supporting our clients through the industry reset, both for today and the future.

- Grape Market 3

- North Coast 3

- Central Coast 3

- San Joaquin Valley 4

- Bulk Market 4

- Cabernet Sauvignon 5

- Chardonnay 5

- Pinot Noir 6

- Conclusion 6

- Crop Contest 7

- Turrentine on the Road 7

- Market Opportunities 8

As harvest ramps up, opportunities are available across the state. From premium Napa Valley Cabernet to versatile red blenders and new plantings, here’s a quick snapshot of the grapes currently available on the market. Please reach out to our brokers for more details.

Napa Valley

• Cabernet Sauvignon

• Chardonnay

• Red Blenders

Sonoma County

• Cabernet Sauvignon

• Chardonnay

• Sauvignon Blanc

• Red Blenders

North Coast

• Cabernet Sauvignon

• Chardonnay

• Sauvignon Blanc

• Red Blenders

San Benito County

• Chenin Blanc – small lot or truckload

Monterey County

• Grenache – new, but established planting; very uniform; suitable for red or roséPaso Robles

• Cabernet Sauvignon – multiple locations and clones available; nearly every appellation

San Joaquin Valley

• Cabernet Sauvignon

• Chardonnay

• Merlot

• Zinfandel

• Sauvignon Blanc

Let’s make a match.If any of these opportunities align with your buying needs, get in touch with your Turrentine broker today. We’re here to help you find the right fruit, right now.

Navigating Uncertainty

by Steve Fredricks

"Uncertain" is the word most people are using to describe the current wine market. This sentiment applies to everything from the long-term outlook for wine consumption and vineyard acreage, to the projected size of the 2025 harvest and the immediate future of the bulk wine market. These inherent market uncertainties are further complicated by external tariff and trade issues impacting the broader economy.

This cloudy picture has led to delayed decision-making, with bulk wine and grape purchases remaining conservative. Buyers are cautious when adding additional inventory, resulting in soft bulk wine and grape prices. This oversupply cycle is proving to be the most challenging the industry has faced in decades.

Despite the persistent oversupply and low prices, the market is evolving, particularly on the supply side. We're seeing vineyard acres removed or unfarmed, bulk wine sold at low prices, and exciting innovation in wine styles and price points aimed at capturing consumer attention. While these efforts by growers and wineries are undoubtedly reducing supply, their full impact has yet to be reflected in the market.

The following update aims to bring some clarity to the bulk wine and grape markets by highlighting these supply-side adjustments and illustrating how the wine business is working to navigate this challenging cycle.

- Bulk Market 3

- Cabernet Sauvignon 3

- Chardonnay 4

- Pinot Noir 4

- Pinot Grigio 5

- Sauvignon Blanc 5

- Grape Market 5

- North Coast 6

- Central Coast 6

- San Joaquin Valley 6

- Conclusion 7

- Turrentine on the Road 7

- 2024 Crop Contest Results 8

- Market Opportunities 10

Our latest Sustainable Winegrowing podcast episode brings together two of Turrentine Brokerage’s leading experts—Audra Cooper, Director of Grape Brokerage, and Eddie Urman, Central Coast Grape Broker—to explore how the wine industry can navigate a market defined by oversupply, shifting demand, and the growing push for sustainability.

Our latest Sustainable Winegrowing podcast episode brings together two of Turrentine Brokerage’s leading experts—Audra Cooper, Director of Grape Brokerage, and Eddie Urman, Central Coast Grape Broker—to explore how the wine industry can navigate a market defined by oversupply, shifting demand, and the growing push for sustainability.

Listen to the full episode

Play Episode 269: From Surplus to Strategy

Meet Your Hosts

Audra Cooper

With nearly two decades at Turrentine Brokerage, Audra leads our grape brokerage team. A Central Coast native with a background in Agricultural Economics (CSU Fresno) and strategic management, Audra champions data-driven strategies to keep clients ahead of market shifts.

Eddie Urman

A Paso Robles native and Cal Poly alum, Eddie brings over ten years of vineyard management and brokerage experience to his role as Central Coast Grape Broker. Known for his deep grower relationships and hands-on market analysis, Eddie helps clients turn changing supply and demand into opportunity.

Key Takeaways

- Understanding Oversupply

The current climate of surplus fruit calls for creative solutions—bulk wine trades, multi-year contracts, and strategic vineyard removals to rebalance supply. - Sustainable Certification as a Business Lever

Buyers increasingly require SIP or other sustainability certifications. Not being certified can immediately halve your potential buyer pool. - Regional Dynamics Matter

Varied growing regions face unique challenges—from water stress in the Central Coast to labor concerns in the North Coast—requiring tailored brokerage approaches. - Innovate Through Collaboration

Industry partnerships, shared research, and marketing alliances strengthen resilience against market fluctuations. - Future Trends

Bulk wine market shifts, consumer preference for sustainably produced wines, and digital matchmaking platforms are all set to redefine brokerage in the coming years.

Why It Matters for Growers & Wineries

In an industry where planting decisions happen years before harvest, staying ahead of market trends is non-negotiable. Audra and Eddie share actionable strategies to:

- Optimize vineyard contracts

- Maximize returns on surplus fruit

- Enhance market access through sustainability credentials

- Build long-term partnerships across regions

Whether you’re a grower planning next season’s tonnage or a winery looking to source quality fruit, this episode delivers the insights you need to turn today’s challenges into tomorrow’s opportunities.